Executive Summary

Over the past two years, the combination of the coronavirus pandemic and a pre-existing push for a shift to renewables has drastically changed the refining economic environment. Specifically, from 2019 to 2022 we have seen:

- Reduction in operable refining capacity (~1,040k bpd or 5.5%)

- The return of fuels demand to comparable or higher levels than seen in 2019

- Refiners who are unwilling to invest in capacity debottlenecks due to shareholder ESG (Environmental, Social and Governance) demands or government policies

These factors have combined to create a unique historical situation where, given what we know today, it is reasonable to expect a prolonged up-cycle in refining due to a capacity shortage that will not be quickly resolved. In the near-term this is further magnified by Russia’s war in Ukraine, which effectively makes much of Russia’s refining capacity unavailable as western nations snub or sanction Russian refined product and oil supply.

Unlike higher margin (although nothing has been seen like the current $50+ crack spreads) periods in the past wherein investment in refining capacity was spurred, this investment from publicly held companies is much less likely to happen this time around due to ESG investing and activist investors. Planned capacity additions that we are aware of are only set for the eastern hemisphere, leaving a large arbitrage requirement to see those barrels come to the US (essentially another factor that should help to bolster US refining spreads for some time).

Refining Capacity Lost

The US refining industry collectively lost several sites during the pandemic downturn. In the US, these closures total to over 1 MMBPD as shown in the chart below. I have also listed several specific sites and what led to their closure or potential closure as refining sites. Some are being repurposed as terminals or renewable diesel units (at a much lower capacity and needing to secure their bio-oil feedstocks).

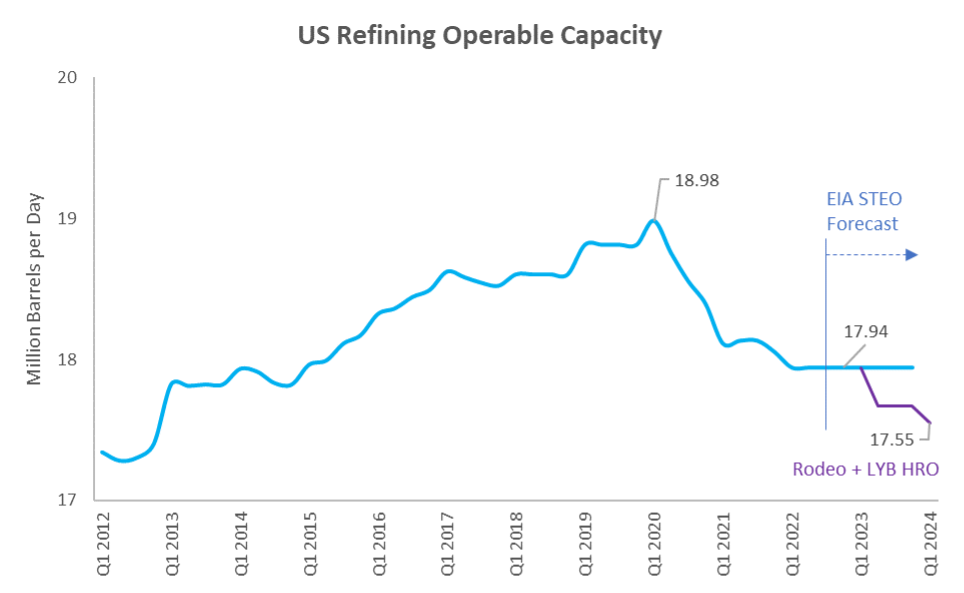

Fig 1: After Q1 2020, over 1 million barrels per day (5.5%) operable distillation capacity has been lost in the USA. Source: EIA Short Term Energy Outlook 2022 (STEO)

| Site | Crude Capacity (bpd) | Closure Reason / Plans |

| P66 Alliance, LA | 250,000 | Hurricane Damage, economics – unable to find a buyer to operate, reusing as a terminal |

| Philadelphia Energy Solutions, PA | 335,000 | Process safety incident, economics – purchaser to redevelop as non-industrial use? |

| Shell Convent | 211,146 | Economics during Covid, Shell aspirational transition out of refining – unable to find a buyer to operate |

| Marathon Martinez, CA | 161,000 | Economics during Covid, ESG push – terminal / transition to renewables |

| HollyFrontier Cheyenne, WY | 48,000 | Conversion to renewable diesel |

| Marathon Gallup, NM | 27,000 | Not known, presumably economics during Covid |

| Marathon Dakota Prairie, ND | 19,000 | Economics, conversion to renewable diesel |

| LYB Houston, TX | 268,000 | 2023 SD: Planned SD if not sold per LYB press release, aspirational focus on chemicals/polymers business |

| P66 Rodeo, CA | 120,000 | 2024 SD: Planned conversion to renewable diesel only |

| Total Including Future SD | 1,439,000 |

Fig 2: Refinery closures 2019 to current, including two future closures that have been announced. Various sources.

Currently, the Ukraine war has also resulted in shifts in how distillates and oil are supplied to the world, likely a transient, but long duration impact to refining margins on top of the already tight supply situation. EU has greatly increased its demand for US oil and distillate exports.

Demand Returned and Continues Growth despite Electrification Aspirations

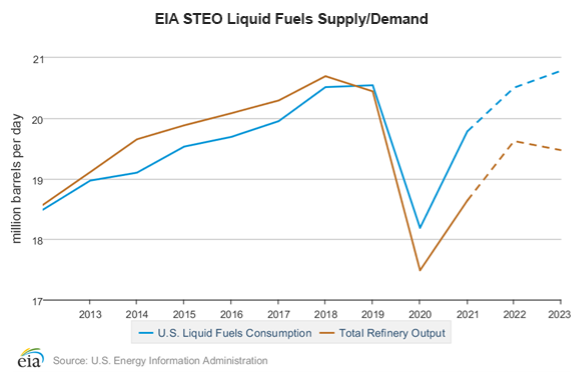

In the EIA short term energy outlook (STEO), fuels demand returns to and exceeds pre-Covid demand by 2023 as shown in the chart below generated from the 2022 EIA STEO data. On the other hand, refining capacity is quite impaired by closures/conversions. While renewable diesel will help to make up some portion of the lost fuels production, the capacity of the renewable unit(s) are usually a fraction of the original crude processing capacity.

Fig 3. US total refinery falls below US liquid fuels consumption 2019 and beyond. As noted in an earlier plot, this projection does not include the potential LYB HRO and P66 Rodeo shutdowns. Source: EIA STEO 2022

A basic understanding of economic fundamentals will tell you that the chart above is not really feasible in the context of limited sources of imports to fill the gap (in fact, we are a significant exporter of fuels to Latin America and now at least temporarily to EU). The price of the products will theoretically have to rise enough to destroy some of the elastic demand such that it matches the available supply. This environment is primed for maintaining higher than typical margins.

For more information, visit imubit.com

Recent Posts

Jun 30, 2025