Second wave of COVID increases risk for already challenged refiners

Over the last several weeks, we have once again seen COVID-19 cases in the US (and globally) rise significantly. In the initial stages of the outbreak the primary tool that governments had to address the spread of the disease was to implement various degrees of lockdowns which resulted in lower economic activity and energy demand.

With the fresh increase in daily cases in October and early November, we are starting to see governments take some of those same actions again, such as the “Lockdown 2.0” that is occurring in the UK (https://www.bbc.com/news/uk-politics-54766061).

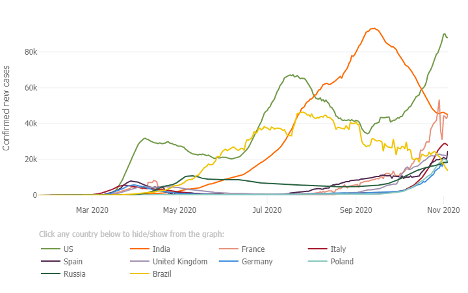

Figure 1: Confirmed COVID cases are trending up in many countries, increasing risks of additional shutdowns, such as we have seen in the UK. (Credit: John Hopkins University https://coronavirus.jhu.edu/data/new-cases)

I do think there is some reason to be a little more optimistic this go around, as we do understand the spread of the disease much more and most communities have mandatory masking in place – I think there is some reason to believe that not all countries seeing an increase will move back to the same kinds of lockdowns we saw in April. Combine that with the outlook to begin vaccinations in some countries soon (maybe within a month from now), and the outlook is less bleak than it was.

That said, the numbers are the numbers, and spread IS occurring currently so there will likely be actions taken that decrease transportation fuels demand. This most definitely means a trip back down to (or staying at) lower utilization rates, and a continued lack on incentives to run outside of conversion tiers.

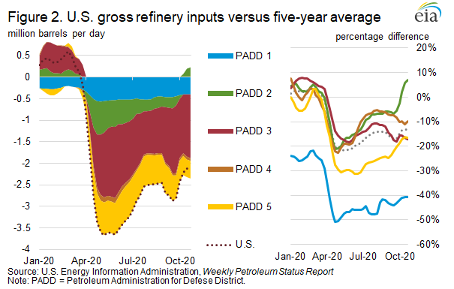

Figure 2: EIA analysis of refinery inputs since the beginning of this year (https://www.eia.gov/petroleum/weekly/)

One interesting point is that PADD2 (US Midwest) is above its five-year average for this time of year. Given their supply of local markets, the fall harvest, and closer proximity to Canadian heavy crude is likely helping to power this. PADD3 must pay pipeline tariffs in both directions to supply their market, so PADD 2 is pretty safe.

If we do revisit the lows of April-May this year, we might see some refineries just shut down for extended turnaround (TAR). Many have already kicked the can down the road, but deferred maintenance will force you to TAR at some point. Depending on the mid-term outlook we could definitely see more rationalization of capacity as well.

It will also be interesting to see how gasoline and diesel demand relative to each other shake out – harvest season and floating storage loading have propped up diesel for now, and in the wintertime diesel is generally higher than gasoline, thanks to heating oil demand and less demand for gasoline. On the downside for diesel, it trends with GDP, so if world economies dip again demand would falter.

One thing is for sure, refining margins will continue to be low and volatile for the foreseeable future. The value of yield optimization, while lower than when there are large spreads, is still there and is now more dynamic. Some optimizations like FCC volume gain and hydrocracker yield are always at play, and when octane is not highly valued, minimizing reformer octane to the bare minimum needed to produce feasible blends can pay in additional barrels of sellable product (or less refinery inputs).

See imubit.com for more details.

Recent Posts

Jun 30, 2025