Energy Transition accelerated in EU and USA by Covid-19 resulting in peak Mogas demand, other regions to keep oil demand growing for some time

In this month’s economic engineering update, we zoom out for a look at the global supply and demand environment for oil, transportation fuels, and petrochemical feedstocks. The Covid-19 pandemic caused a huge dent or “reset” in oil product demand which has sent ripples through the markets. The changes caused by Covid-19 extend far into the future due to some likely irreversible changes and trends toward reducing the effects of climate change. These changes came about through the insistence of individuals (e.g., telecommuting trends), the private sector (ESG push), activists (continued pressuring of governments and other entities), and government action.

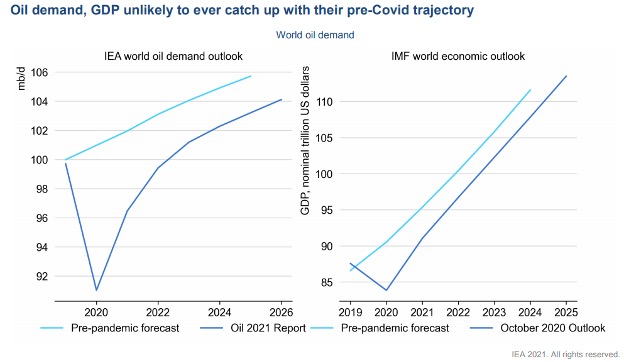

Much of what we will discuss today will be backed up by projections and figures from the IEA (International Energy Agency) and their Oil 2021 forecast1. I highly recommend giving it a read if you are interested in views on the macroeconomic environment and supply/demand impacts. I have pulled out a few of the key insights that I see affecting the refining and petrochemical industries. First let’s take a look at the projection for total oil demand, which includes all end-uses in figure 1 below.

Figure 1: IEA projection of world oil demand alongside Gross Domestic Product (GDP). They project the world will not return to the original trajectory.1

This graph most prominently shows the permanent economic scarring due to the pandemic. Global GDP is now expected to be on a different curve, although still rising healthily. Baked into forecast oil demand are the shift towards EVs, a sudden increase in work from home, and likely a permanent change in how business is conducted in the developed world. Some of these trends were accelerated by the pandemic.

No Peak Oil, but we have seen Peak Gasoline

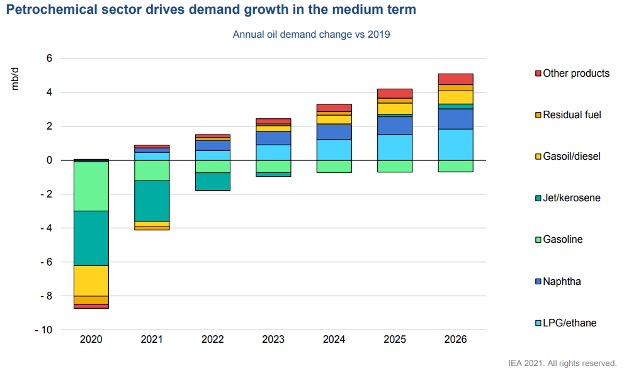

The next point I would like to highlight is where the increase in global oil demand is expected to go – and by the IEA’s projection, it will not be into gasoline. Chemicals is seen as the primary driver of demand growth in the medium-term projection.

Figure 2: Gasoline world demand remains below 2019 levels through 2026, new oil demand arises from petrochemical end uses and diesel.1

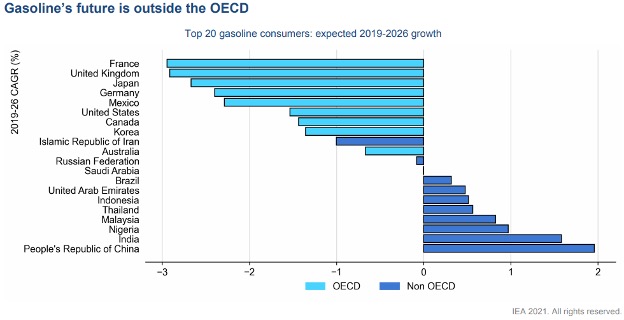

So, we have established at this point that we have not yet seen “peak oil” as the IEA projects it, however; what we do see in Figure 2 and Figure 3 below, is that we have seen peak gasoline in 2019. The OECD countries are already in demand decline, which will be accelerated by EV adoption, behavioral changes, and efficiency increases. Even with strong EV adoption (expected to triple by 2026) in China, there is still a slight uptick in gasoline demand there.

Figure 3: Much of the OECD (Organization for Economic Co-operation and Development) countries have already seen peak mogas demand, growth is primarily in non-OECD countries.1

The above transition as well as global oil production and refining footprints will dictate continued shifts in trade flows, promoting additional gasoline exports from NA and EU refiners. Eventually if capacity continues to be expanded in Asia/Middle-East/Africa, there will likely be more capacity rationalization in the NA/EU.

Jet back to normal by 2024

While jet will certainly not be much of a growth potential, IEA sees it returning to normal by 2024 and then increasing at a slow pace afterward. This does mean a couple more years of relatively low Jet vs. Diesel margins.

Diesel shifts geographies similar to Gasoline

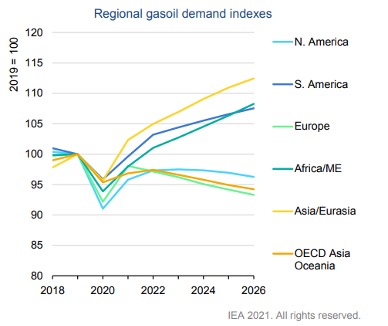

Unlike gasoline, the IEA does not see diesel demand peaking yet. As shown below in figure 4, it is expected to increase in some regions, offsetting efficiencies in others. Diesel is much harder to replace with battery electric due to the high energy density required. Blue and Green H2 is being talked about as a solution for this but being a practical and scalable alternative is still to be demonstrated and scaled.

Figure 4: Regional gas/oil demand indexes show growth in diesel shifting to Asia/Africa/ME/South America. EU, NA, and OECD Asia are all projected to decline.1

Hydrocarbon processors globally, particularly refiners, will be in a period of flux for the mid-term as the course to decarbonization becomes clearer. The market dynamics will be interesting as supply and demand will be displaced geographically. Refiners will need to be able to respond to open arbitrages quickly to capture the opportunities which might mean switching from diesel to gasoline quickly and potentially counter seasonally at times.

The best operators will take this future into account and prepare themselves to be more nimble, more profit-driven, and more capable. Imubit can help with these changes with our Closed Loop Neural Network™ platform. We help organizations to respond quickly to changes in market signals and enact optimizations that were not previously feasible.

1 IEA (2021), Oil 2021, IEA, Paris https://www.iea.org/reports/oil-2021

For more information, visit imubit.com

Recent Posts

Jun 30, 2025